Subsale vs New Launch in Malaysia: Which One Is Actually Worth Your Money?

Thinking of buying property in Malaysia? Here's an honest breakdown of subsale and new launch pros, cons, and hidden costs — so you don't learn the hard way.

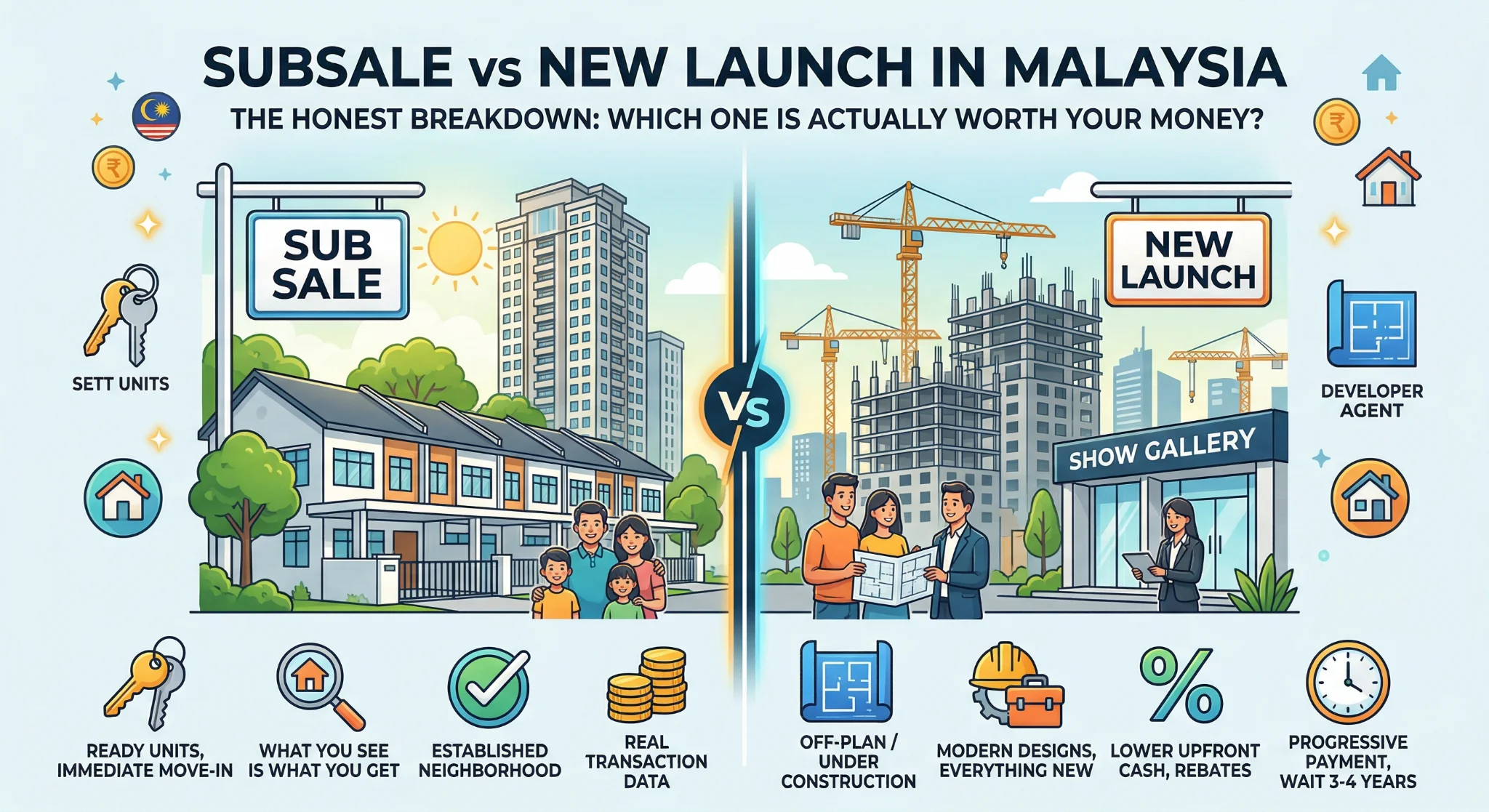

Let's be real — if you've spent any time browsing property in Malaysia, you've probably noticed two very different worlds.

On one side, you've got new launches — showrooms with mood lighting, scale models under glass, and salespeople who make everything sound like the deal of the century. On the other, there's the subsale market — real units you can actually walk through, with actual neighbours and actual wear-and-tear.

Both have their place. But choosing between them isn't as simple as "new is better" or "subsale is cheaper." The right answer depends on your timeline, your budget, and honestly — how much risk you're comfortable with.

Let's break it down.

What Exactly Is a Subsale?

A subsale (also called a secondary market purchase) means you're buying from an existing owner — not from the developer. The property is already built, and in most cases, already occupied or rented out.

You're essentially buying someone else's property. The unit exists. You can touch the walls, check the water pressure, and peek at the neighbours' shoes outside the door.

And a New Launch?

A new launch (or primary market) means you're buying directly from the developer, usually before or during construction. You're buying based on a floor plan, an artist's impression, and a promise.

Some new launches are completed stock — already built but unsold. But most of the time, when people say "new launch," they mean buying off-plan. You pay progressively as construction milestones are hit, and you collect your keys 3–4 years later.

The Price Question Everyone Asks

Here's the thing people get wrong: new launches aren't always cheaper.

Developers price new projects based on future value — what they think the area will be worth when the project completes. They factor in their land cost, construction cost, marketing budget (those showrooms aren't free), and profit margin.

Subsale properties, on the other hand, are priced by the current market — what buyers are actually willing to pay right now, based on recent transactions and comparable sales.

A Real Example

Let's say you're looking at a condo in Bangsar South:

| Subsale Unit | New Launch Nearby | |

|---|---|---|

| Size | 900 sqft | 850 sqft |

| Price | RM 580,000 | RM 650,000 |

| PSF | RM 644/sqft | RM 765/sqft |

| Completion | Move in now | 2029 (est.) |

| Rental income | Immediate | 3–4 years away |

The new launch costs more per square foot, and you can't use it for years. But the developer might throw in freebies — legal fees absorbed, stamp duty rebates, free kitchen cabinets, that sort of thing.

The subsale is cheaper on paper, but you'll pay your own legal fees, stamp duty, and probably some renovation to bring it up to your taste.

Neither is objectively "better." It depends on what you need.

The Honest Pros and Cons

Why People Choose New Launches

The good stuff:

- 🏗️ Lower upfront cash — Developers often absorb legal fees, stamp duty (partially), and MOT fees. Some even offer rebates on the down payment

- 📋 Progressive payment — You don't pay the full amount upfront. During construction, you pay in stages (typically 10% booking + progressive billing)

- ✨ Everything is new — No previous owner's questionable renovation choices. Fresh fittings, new plumbing, modern layouts

- 📈 Potential capital appreciation — If the area develops as expected, your property could be worth more by the time it's completed

- 🔒 Developer warranty — Defect liability period (usually 24 months) means the developer has to fix structural and material defects

The not-so-good stuff:

- ⏰ You're waiting 3–4 years — That's 3–4 years of not living in it and not earning rental income. If you're currently renting, that's potentially RM 60,000–100,000+ in rent you're paying while waiting

- 🎲 You're buying a promise — The show unit looks amazing. The actual unit? Sometimes... less so. Finishing quality varies wildly between developers

- 📉 Market risk — A lot can happen in 4 years. The area might not develop as planned. Property prices could dip. Interest rates could spike

- 🏚️ Abandoned projects — It's rare, but it happens. Some projects get delayed by years or abandoned entirely. Your money is stuck

- 🏘️ Cookie-cutter layouts — Everyone in your block has the same floor plan. Standing out for resale is harder

Why People Choose Subsale

The good stuff:

- 👀 What you see is what you get — You can physically inspect the unit. Check for cracks, water damage, noisy neighbours, parking situation, everything

- 🏠 Move in fast — Typically 3–4 months to complete the sale. No years of waiting

- 💰 Rental income from day one — If you're buying as an investment, you can start earning immediately

- 📊 Real transaction data — You can check what similar units actually sold for (tools like Homilens let you see real PSF data and transaction history)

- 🏘️ Established neighbourhood — You know exactly what the area is like. The schools, traffic, restaurants, facilities — it's all there already

- 🔧 Previous owner upgrades — Sometimes you inherit expensive renovations (built-in wardrobes, extended kitchen, air-con units) at no extra cost

The not-so-good stuff:

- 💸 Higher upfront costs — You pay stamp duty, legal fees, valuation fees, and agent commission (usually 2–3%) yourself. This can add RM 20,000–40,000+ to your total cost

- 🔨 Maintenance and repairs — Old plumbing, aging wiring, worn-out air-con units. These costs add up

- 📝 More paperwork complexity — Subsale transactions involve more parties (seller, buyer, both banks, both lawyers). More things can go wrong or get delayed

- 🏦 Bank valuation risk — If the bank values the property lower than the agreed price, you have to cover the difference in cash

Hidden Costs Most People Don't Talk About

This is where people get caught off guard. The sticker price is never the full price.

New Launch Hidden Costs

| Cost | Amount |

|---|---|

| SPA legal fees | Often absorbed by developer |

| Loan legal fees | RM 3,000–8,000 (sometimes absorbed) |

| Stamp duty (SPA) | Sometimes partially absorbed |

| Stamp duty (loan) | RM 2,000–5,000 |

| Renovation & furnishing | RM 30,000–80,000 (bare unit) |

| Rent while waiting | RM 1,500/mo × 36 months = RM 54,000 |

| Realistic total extras | RM 50,000–140,000 |

Subsale Hidden Costs

| Cost | Amount |

|---|---|

| SPA legal fees | RM 5,000–12,000 |

| Loan legal fees | RM 3,000–8,000 |

| Stamp duty (SPA) | 1–4% of purchase price |

| Stamp duty (loan) | 0.5% of loan amount |

| Agent commission | 2–3% of price (paid by seller, but priced in) |

| Valuation fee | RM 1,000–3,000 |

| Minor renovation | RM 5,000–30,000 |

| Realistic total extras | RM 30,000–70,000 |

Notice something? New launches look cheaper upfront, but when you add the opportunity cost of rent during the waiting period, the gap narrows significantly — or even flips.

The Developer Factor

Not all developers are equal. This matters enormously for new launches.

Tier-1 developers (think S P Setia, Sime Darby, Gamuda, Mah Sing, IOI) generally deliver on time and to a reasonable standard. Their projects tend to hold value.

Smaller developers can be hit or miss. Some deliver incredible value. Others cut corners on finishing quality, delay completion, or underdeliver on promised facilities.

Before buying a new launch, always:

- Check the developer's track record — how many projects completed on time?

- Visit their completed projects (not the showroom — the actual buildings)

- Talk to residents who've lived there for 1–2 years

- Check the developer's financial health

For subsale, the developer matters less — you're buying a finished product. Focus on the management body, maintenance quality, and sinking fund health instead.

Which One Is Better for Investment?

If you're buying purely for returns, subsale usually wins — but not always.

Subsale Investment Case

- Immediate rental yield (typically 3–5% in KL)

- Known rental demand (you can check current listings in the building)

- Shorter holding period before returns kick in

- More predictable cash flow

New Launch Investment Case

- Potential for below-market entry pricing (early bird discounts)

- Capital appreciation during construction ("buy at RM 500k, worth RM 600k on completion")

- Lower cash outlay during construction period

- But: zero income for 3–4 years, and the appreciation is never guaranteed

Here's a simple calculation:

Subsale: RM 500,000 condo, immediate rental at RM 2,000/month

- After 4 years: RM 96,000 rental income earned

- Even with flat capital value, you're RM 96,000 ahead

New Launch: RM 480,000, completed in 4 years, sell at RM 560,000

- Capital gain: RM 80,000

- Rental income during construction: RM 0

- Rent paid while waiting (if applicable): -RM 72,000

The math often favours subsale for cash-flow investors. New launches work better if you're betting on specific area growth and don't need immediate income.

So, Which Should You Choose?

Choose Subsale If...

- ✅ You need a place to live within the next 6 months

- ✅ You're buying for rental income

- ✅ You want certainty — you need to know exactly what you're getting

- ✅ You prefer established areas with proven demand

- ✅ You have a comfortable cash buffer for upfront costs

Choose New Launch If...

- ✅ You're 3–5 years away from needing the property

- ✅ You want lower upfront cash commitment

- ✅ You're targeting an up-and-coming area (near new MRT station, new township development)

- ✅ You're buying from a reputable developer with a strong track record

- ✅ You want a brand new unit with modern layouts and fittings

Avoid New Launch If...

- ❌ The developer has a history of delays or quality complaints

- ❌ The area has oversupply issues (check completion pipelines — NAPIC data helps)

- ❌ You're stretching your budget and can't afford to wait

- ❌ The pricing is significantly above current subsale PSF in the same area

The Bottom Line

There's no universal right answer. People who bought subsale in Bangsar 10 years ago did great. People who bought new launch in Cyberjaya in 2015... not so much.

The key is to forget the sales pitch and look at the numbers:

- What's the actual PSF compared to surrounding subsale properties?

- What's the realistic rental yield after all costs?

- Can you afford the total commitment, including the hidden costs?

- What's your timeline — do you need this property now, or is it a long-term play?

Use transaction data to make your case. Check what similar properties actually transacted for — not what they're listed at. Tools like Homilens give you access to real transaction histories, PSF trends, and neighbourhood data across Malaysia.

Don't rely on anyone else's opinion about "good investment." Run the numbers yourself. That's how you avoid buying someone else's mistake.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Property markets involve risk, and past performance does not guarantee future results. Always consult a licensed professional before making property purchase decisions.

Written by

Homilens Team